The essential event in 2013 – evacuation of the Schibsted Concern

Eduardas EIGIRDAS

Scandinavian banks dominate the Baltic countries, using controlled capital and experience, while a high number of powerful media groups in Scandinavia and those controlling huge capital and having unique experience are abandoning positions in Latvia, Lithuania and Estonia one by one.

This trend is alarming, as the transparent media market is no less important than the transparent and competitive banking market. If the Nordic entities are leaving because of the negative perceptions being characterised in the media, in the long run, this may have a negative impact on the economies and politics of the Baltic countries. Unfortunately, in order to grasp the nature of media processes in the Baltic countries, one must not focus on the information provided by Scandinavian entities about the market specifics and reasons for their withdrawal, as most comments are very brief. We should also remember that these large entities were entering Estonia, Latvia or Lithuania with their heads held high, and had very ambitious goals, while their withdrawals were modest and quiet.

Orkla Media left in 2006

The first, over the past decade, that decided to withdraw from the Baltic media market was a Norwegian concern, Orkla Media. In 2006 it sold 100 per cent of its shares in the most solid and influential regional newspaper in Lithuania, Kauno diena, controlled since 1998, to the British Mecom investment fund. This withdrawal surprised many because at the time, no one thought of the impending crisis, and the years of 2006, 2007 and even 2008 were most successful for the Lithuanian media. Thus, unexpected changes in the economy could not be the reason for withdrawal. In any case, you can agree with Assoc. Prof. Dr. Deimantas Jastramskis, director of the Institute of Journalism of Vilnius University, who says that purportedly, the sale of the Kauno diena daily newspaper meant nothing for such a powerful concern as Orkla. But this is true only in terms of financial results and not strategy. When investing in the Baltic media market, Scandinavian concerns were perfectly aware that the turnover and profits here would be far lower than in the major markets. But they invested because it was a logical strategy of expansion to neighbouring markets. However, it suddenly changed. For as yet undisclosed reasons, instead of a desire to expand further, a desire to return home emerged.

When trying to understand the real causes of withdrawal of the Nordic entities, we should not speculate on what factors led to such changes in the strategy, but instead consider who replaced them. After all, what replaces the Scandinavian media groups and takes over their newspapers points out the real forces, the development of which is one of the reasons why the Scandinavian concerns capitulated. Thus, the British investment fund Mecom has become just a beautiful sign bought because the Kauno diena daily was fairly quickly passed on to the hands of Lithuanian businessmen. They played with it a little, separated the activities, disposed of the immovable property and sold the newspaper, now impoverished in terms of capital, to a company controlled by an even more distinguished businessman, banker and Lithuanian People's Party founder, Vladimiras Romanovas. It was Ūkio Bankas, managed by his banker, which was suspended in the beginning of 2013 by the Central bank of Lithuanian, and at the time of writing this article, the banker still had not returned to Lithuania from Russia. Although Lithuanian prosecutors are eager to question him, as stated by representatives of the Lithuanian Prosecutor General's Office, the former owner of Ūkio Bankas, V. Romanovas, is suspected of high-level bank embezzlement. Therefore the Orkla concern, with such a beautifully idyllic beginning, withdrew, and today one of the major and once a very objective daily newspaper is weak, to say the least, while a fight is going on backstage for its control. According to other sources of the editorial board, the main fighting forces can be characterized as follows: the supporters of the banker are hiding in Russia, in the region of largest electricity supplier, partners of the Russian giant, Inter RAO in Lithuania.

Looking at what happened to the Kauno diena daily, one can say that the powerful Norwegian Orkla concern retreated, and left one of the highest quality Lithuanian daily newspapers to be torn to shreds. Without a doubt, it would be irresponsible to say that the Norwegian entity representatives could have foreseen these consequences. However, it is clear that the desire of local business groups to take control of the media was significantly higher than the willingness of the Scandinavian concern to stand its ground.

Bonnier has an economic alibi

The Bonnier Group is a Swedish family business focused of the publication of books and magazines, business press, newspapers, broadcast operations, and other media. When Gerhard Bonnier opened a small bookstore in Copenhagen in 1804, he could not dream that after 200 years his small business would turn into an international corporation. In 2012, Bonnier employed 10,176 personnel, the group owned 175 companies operating in more than 17 countries, and their sales amounted to 29.176 billion Swedish crowns.

Bonnier is the only major Scandinavian media entity whose withdrawal can be justified in part by the crisis. In 2009, at the very peak of the crisis, it withdrew from Latvia. As was reported by the media at the time, the Swedish press publisher, Bonnier Business Press, sold its business in Latvia – Diena publishing group, publishing a daily newspaper under the same name, and the Dienas Bizness business newspaper. It was purchased by the Latvian company, Nedela S.A., for an undisclosed price. It was also announced that the Nedela Company is financed by Luxembourg Financial Services, established and managed by a group of wealthy businessmen in Estonia. Bonnier reportedly stated that the deal was initiated by Nedela. On this occasion, the board chairman of Bonnier, Casten Almqvist, said: “Nedela gave us an offer that satisfied us and was beneficial. This transaction will allow us to further consolidate our position in priority markets such as Scandinavia, Russia, Estonia, Lithuania, Poland, Bulgaria and Slovenia”. Therefore, according to this report, it is quite surprising that one of the most powerful Swedish concerns decided that Bulgaria and Slovenia are priority markets, but Latvia – no longer is. This evolution can only be explained by Bonnier’s desire to keep the positions achieved in the Latvian market significantly lower than the willingness of potential investors to take them over, at some point.

What has this meant to the Latvian media market and what impact has this had on Latvia as a state? From 1993 to 2009, Latvia's largest national daily, Diena, owned by Bonnier, earned the reputation of a prestigious, liberal and western-minded daily. After the change of shareholders, it quickly diminished, and its main editors and journalists left the newspaper. A mysterious transaction of an undisclosed amount, which, according to the Estonian portal aripaev.ee could have been as much as 44.9 million lats, fuelled speculation and rumours about where the shares of the daily newspaper ended up. An investigation of the Latvian Corruption Prevention Office revealed that the newspaper is controlled by three politicians. By the way, when we use the phrase “mysterious transaction”, we mean that in the beginning, as in the case of Kauno diena, the Brits were involved in the acquisition process. Because it was namely the Brits, Jonathan and David Rowland, that were named as the new owners of the newspaper. However, after a year, 51 percent of Diena shares were held by a Latvian businessman, Viesturs Koziol, and in 2012 he already owned 98.86 percent of the holding. Nevertheless, as mentioned above, the investigation of the Corruption Prevention Office found that the actual owners of the newspaper are three politicians.

So, based on this information, it can be assumed that the Scandinavian concern in Latvia, as in Lithuania, handed over the influential media to persons willing to pay a relatively high price because they needed influence. And that is not good, because when a young country experiences the growing influence of those to whom the media is not a business, but a tool being used to influence political and economic processes, this does not yield anything good for the state or its business. Scandinavian entrepreneurs probably do not have to be advised how the business environment in Sweden and Norway might change, if their main newspapers are acquired by populist political party founders or entrepreneurs associated with Russia. It goes without saying that this would have a negative impact on both society and business. Therefore, the withdrawal of the major Scandinavian concerns is not to be seen as a business transaction, but rather capitulation, when it is recognised that changing the business environment in the media, ensuring a more transparent media market and information environment is difficult, and withdrawing and giving away the market to those who need it, it is a lot easier. Of course, for the purposes of objectivity one can also consider the version that the Swedish concern Bonnier, with short-term assets amounting to about 7.5 billion Swedish crowns in 2013, sold the Diena and Dienas Bizness newspapers because both publications had experienced 1.78 million and 6.3 thousand lats of loss, respectively, in 2008. However, publications of the Bonnier Group also suffered losses in other countries during the crisis. In Lithuania, for instance, the Verslo žinios group it controlled, publishing a daily under the same name, operated at a loss for at least several years in succession. However, the Bonnier Group did not sell publications in Lithuania or Estonia. Therefore, one has to choose whether we should believe the statements that these publications are not sold because the markets are strategic, or simply draw attention to the fact that in these countries, the Bonnier Group does not own media that has a significant impact on society. Therefore, for those who collect influence, these publications controlled by the Bonnier Group are not valuable enough to pay for them so that the offer satisfies Bonnier.

Schibsted were the last to decidedly capitulate

Oslo-based Schibsted is one of the largest media groups in Scandinavia and has been operating since 1839. Not only does it own press companies, but also TV channels, movie, publishing and mobile services companies. Schibsted employs more than 7,800 personnel. The concern operates in 29 countries, is well established in Scandinavia, in many countries of Europe, Latin America, Asia and even in Africa (Morocco). According to the financial statements of 2012, Schibsted operating income amounted to 14.763 million Norwegian crowns.

While analysing Schibsted's withdrawal, we were surprised to find that this media group, which operated in Estonia since June 1998 and controlled the country’s largest media holding, Eesti Meedia, was still expanding as late as in 2011. It was the year when a subsidiary of the Schibsted Media Group acquired 100 percent of the second biggest news portal in Latvia, tvnet.lv. The director general of Eesti Meedia managing this investment of Schibsted, Mart Kadastiku, called this a significant step towards expansion into the Baltic countries. The development process in Lithuania took place fairly recently and was distinguished with its short-term determination to achieve results. The companies managed by this concept made attempts to establish themselves in the market of daily newspapers twice. Initially they purchased the Ekstra žinios newspaper, attempted to establish themselves with it, and after failing, purchased the freely distributed and promising 15 min newspaper. After a few years it became a weekly, and then disappeared completely, just like Ekstra žinios. Yes, they still have the Internet portal, which is currently the second most popular in Lithuania.

So, the concern that has been pursuing expansion back in 2006 in Lithuania and in 2011 in Latvia, said they realise that they have to concentrate on larger markets and pursue the classified advertising business, therefore they sold their business in the Baltic States to the managers of the Eesti Meedia group and to the host of UP Invest, one of the wealthiest people in Estonia, the pharmaceutical tycoon, Margus Linnamäe. As reported, he offered to buy the shares because he had heard rumours that allegedly, Gazprom intended to buy the Estonian media concern. One can only be glad that the retreating Schibsted was not replaced by Gazprom, but what it has left behind will only be seen after a few years.

The rapid development of Schibsted and very quick retreat, when the business was sold to Eesti Meedia for 30 million euro (they say this transaction resulted in a 26 million euro loss) is surprising, but even more surprising is that in all cases, the major Scandinavian concerns were replaced by influential local businessmen. Somehow they do not try to buy the Scandinavian banks or other companies, but quickly purchase companies that control the media, and especially influential newspapers. By the way, when we are talking about newspapers and their specifics, one should consider that in the opinion of some of the experts, they are much better suited to influence citizens’ opinions compared to the TV, let alone the Internet. Therefore, national and regional newspapers are the targets of entrepreneurs combining major political and business interests. Their control can have a significant impact on the election results, and through them – on all processes going on in the state. For this reason, to achieve certain goals through the media, business groups tend to pay more for influential daily newspapers than they are worth.

Why did the Scandinavians run away, and when will they return?

Business efforts to use the media to help win elections to parties that, in return, make beneficial decisions, is a tradition as old as the media itself. However, awareness of this tradition does not answer the question of why the big Scandinavian entities that control the influential newspapers retreated now. This question is best answered by an analysis of the processes taking place in the geopolitical and energy sectors. One can see the trend that with the growth of the Gazprom gas prices, the Baltic countries have experienced growing discontent and the increasing efforts of business groups representing Russia's interests to direct negative public reaction on the right path, thus reducing the possibility for people capable of achieving change detrimental to Gazprom and other Russian energy companies to enter into the politics. For this reason, the influence of the money allocated support of Russia's interests has significantly increased in the Baltic media market. For example, as revealed by the Lithuanian State Security Department, before the advisory referendum on the construction of a new nuclear power plant, funds were granted by businesses representing Russian interests (according to unofficial reports, tens of millions of litas) to turn public opinion against this project. Nevertheless, today Lithuania imports about 70 percent of its electricity, most of it from Russia. Thus, transparent media, which did not participate in assimilating these funds assigned by the Kremlin structures, faced strong competition. In terms of the media revenue from “non-traditional” sources, meaning their influence on viewers or readers, we must understand that the need for these services is never-ending. Therefore, the larger the market share occupied by the media, which, in order to survive, becomes well attached to the proceeds of the sale of their impact on the consumer, the more difficult it becomes for other media to compete by refusing this income. Of course, it is likely that a large part of the Scandinavian political and business elite did not even pay attention to this problem, because media corporations do not boast, while Scandinavia is also dominated by companies that suffice with traditional income.

We write all of this not to complain about how difficult it is for us, as expecting any sympathy or assistance from the pragmatic Scandinavians would be ridiculous, but to at least describe the situation of the media market in the Baltic States, enabling a better understanding of why we see the withdrawal of Scandinavian concerns as capitulation. There are no ideal or 100 percent objective media enterprises, but there are some that take into account national interests and there are others that get extra income because of the nihilistic approach. For this reason, the withdrawal of Scandinavians at a time when Lithuania and Latvia are going through a crucial battle for energy independence (Estonia extracts shale, so its situation is different), is understandable as the process worsens the competitive conditions, however, in the background of the essence of the whole process, such withdrawal can be seen as desertion. Consequently, the number of media enterprises with at least minimum consideration of national interests and the essential mission of the media – to objectively inform society, has declined in the market. Meanwhile, the effect of money from interested business structures has grown significantly. This, no doubt, will have long-term adverse consequences because today, journalists who would like to be employed in media that appreciates their professionalism, rather than in their readiness to splash dirt around when asked, have minimal choices. Therefore, they either adapt or abandon journalism and become spokespersons or employees of public relations agencies.

Let’s forecast the future. In view of the fierce battle for the energy independence of Lithuania and Latvia, competitive media market distortions will be the greatest. Therefore, only the media that will sell themselves to business groups that see the media as a tool of influence and disregard negative financial results will survive, along with the media that will adapt, i.e. concentrate their efforts to establish themselves in business, but do not overdo representing national interests. Quite on the contrary – they will often have a nihilistic approach and thus avoid the risk that their principles can complicate their competitive environment. Therefore, if we are talking about when the Scandinavian concerns could return to the national daily newspaper business of Lithuania, Latvia and Estonia, we should note that this will only happen when the Baltic countries throw off the yoke of Gazprom and Inter RAO and gain energy independence. After all, then it will not be worthwhile to overpay for the media control.

Footnotes

There are three main factors adversely affecting the functioning of the media market: influence of the media by business associated with Russia (both its acquisition and performance through other, mostly financial, means), TNS LT survey quality (as stated in one of the comments), and the issue of the transparency of state orders, which is closely related both to the oligarchic group influence and the quality of surveys.

Today the Baltic market is confronted with a paradoxical situation where Estonian business has the greatest impact on the media. Acting in Lithuania, we have to admit that it is the most popular web portal, delfi.lt, controlled by the Estonian businessman, Hans Luik, which is the mainstream media, so far guaranteeing objective presentation of events taking place in society and preventing other web portals from standing out. For this reason, in our interview with this entrepreneur we asked how he manages to survive in the current market and to preserve the principles and values of the democratic media. By the way, I want to believe that the new Eesti Meedia owners, the largest of which has guaranteed that he has purchased this company to protect the media from Gazprom, will also attempt to do everything possible to prevent at least the Estonian media capital companies from supporting Russian interests and not oppose projects for establishing energy independence.

In this situation, the Scandinavians would have already withdrawn

If we are talking about the processes taking place in recent years in the Baltic media market, one can mention the example of VALSTYBĖ, a magazine of economic and political analysis published in Lithuania. Since almost seven years ago, when we began to publish the magazine, one of our main objectives was the struggle for energy independence from Russia, and during the first two years, we got questions from five companies on our intention of selling our publication. Only one interested person was related to a Scandinavian entity and their interest was very superficial, while that of all the others was very specific. Unfortunately, the links of all those four companies with Russian interests were obvious to our publication, and we refused to sell shares very profitably to protect the magazine’s mission against rape. After six months, we were not surprised at all when, once we decided to fight for energy independence and after we began publishing the magazine, we learned that there are publishers in Lithuania who proclaim themselves to be partners of the British (again the Brits) weekly magazine, The Economist. Their magazine is targeting the same segment of readers as VALSTYBĖ, thus not only reducing the potential income from the sale of magazines but from advertising, which in this segment, given the relatively small layer of wealthy people who are interested in the analysis of economic and political processes, was already limited. Quite soon it became clear that the publishers of this magazine are partners of the main Russian giant, Inter RAO, in Lithuania. Thus, the so-called partners of The Economist became the competitors of VALSTYBĖ, which consistently supported the idea that Lithuania, together with Latvia and Estonia, should seek self-sufficiency in the supply of power, and to reduce the influence of Russia. The company controlled by these partners was officially authorised by Vladimir Putin to sell from electricity from the power plant built in Kaliningrad in the Baltic States and other countries. The ambitions of these players were not limited to the establishment of a single publication for the business segment. Later, they also opened the annual The Economist publication, and the Intelligent Life, Top Gear and L’Officiel magazines. It is interesting that, since the beginning of their publishing, there has not been a year when the publishing house of these magazines has operated profitably. But talking about it is ridiculous, given the fact that while the magazine publisher, Intelligent Media, a subsidiary of Scaent Baltic, was counting losses: in 2012 – 2 million litas (8 percent more as compared to 2011 – 1.85 million litas) – the profits of Scaent Baltic were mainly coming from the supply of electricity from Russia, in 2012 it had 87.258 million litas net profit. To summarize this textbook example, in our opinion demonstrating the competition to be faced by those who do not adapt to the media policies implemented by separate interest groups, and attempt to defend the national interest with integrity, it is necessary to pay attention to one more thing. Lately, Verslo žinios, controlled by Bonnier, revealed the companies selling mostly the electricity of the Russian giant, Inter RAO, and publishing several British magazines, as the Swedish capital investment company, Scaent Baltic. So while it would seem that the competition is going on with the company, whose economic background is based on the trade of electricity supplied by the Russian entity, the official competition is going on with British magazines that are controlled by the Swedish capital company.

Lithuania, Latvia and Estonia trying to learn from B. Obama

Karolis MAKRICKAS

There are fundamental foundations of the welfare state – gas, oil and other natural resources, demonstrating the country's economic potential and growth. What if there were no oil, gemstone mines or automotive concerns to focus on? What would show whether countries such as Lithuania, Latvia and Estonia will flourish in the next 10-15 years, and if the purchasing power of their populations will exceed the European average?

In comparing the U.S. and the European Union (EU) member states, we discover that the number of successful startups in the Old and the New continents differs greatly. After all, the establishment and setting up of young companies generating high added value is one of the indicators that shows further growth of the country's economic potential, the future value of real estate, etc.

While we recognise the resources and energy available to a country as fundamental prerequisites of a welfare state, it is important now that the situation is changing. The growing importance of technology companies and their ongoing research towards a country's economic development is well illustrated by the competition that has gone on for several years between the Apple information technology company and the oil giant, Exxon Mobil, for the title of the most valuable company in the U.S. and in the world.

The list of the most profitable companies includes Microsoft, Facebook, Amazon, eBay and many others which could have only been born in the United States. All of them were once startups. So it is no surprise that U.S. President Barack Obama invites the leaders of these companies for dinner at the White House, and discusses about how to increase the number of companies in the country creating high added value.

Although such a dinner party in 2011 could be considered a public relations campaign to promote the president, it, without a doubt, embodies the trend preferred by the U.S. – to strengthen the community of startups. After all, it is already the strongest in the world, and Silicon Valley is the best place in the world to start a business!

At the beginning of 2012, Obama solemnly signed the Jumpstart Our Business Startups Act (the JOBS Act), which emphasizes that small businesses and the presentation of young startup companies with experienced entrepreneurs and investors promotes the development of new jobs and plays an important role in strengthening the country's economic potential.

Another step in the U.S. is that the Senate is about to push the Startup Visa program, which will allow talented immigrants who have created a business in America to live there. The program developers have also emphasised that the program seeks to encourage U.S. competitiveness in the global economy.

Benefits of startups

Corporate giants such as Google say that startups fuel economic growth and increase innovation, while other information technology companies, such as Microsoft and Apple, are actively investing in startups or acquiring them, so it would be difficult not to notice their impact on the economy.

First, startups spend the money received from investors very quickly for office rent, staff salaries, legal advice and other services, and support the local community. According to various estimates, only 30-40 percent of funds in Europe are invested in startups by local businessmen, while other money comes from abroad. Therefore, the benefits are obvious.

Second, setting up new, high value-added companies is a source of creating better paid jobs, eventually allowing them to retain the most creative people, unlocking their potential and enhancing the national average wage. It is important for all countries that want their citizens to prosper and to stimulate economic growth, especially those who cannot boast of large corporations, such as Siemens, Samsung and GMC.

Different sides of Europe

How is the Spanish capital of Madrid different from Tel Aviv and London? Unfortunately, only London (7th place) and close to Europe Tel Aviv (2nd place) are among the best ten top startups. Other places in the top ten belong to the U.S. and Canadian cities.

The biggest concentration of startups is in the more or less European Silicon Valley in Tel Aviv. Another unique thing is that they do not apply an investment ceiling for startups, so even if you come up with a project costing a zillion dollars, you will be heard. The country has a very strong focus on research, and makes education a priority. So, it is no surprise that as many as 63 Israeli companies are included in the NASDAQ listing (more than Europe, Japan, South Korea, India and China put together!).

A complete opposite of Israel – Spain – cannot boast an abundance of startups (though it has excellent universities, and carries out a lot of EU funded research, etc.). Coincidence or not, Spain is in 136th place by rank in the number of new businesses created in the world out of 185 countries in 2013 (it is predicted to fall to 142nd place in 2014!). By comparison: Lithuania is 105, Latvia 59 and Estonia 50.

In 2013, Spain's unemployment rate for the first quarter was 27 percent. But unlike the U.S., when there are a growing number of startups in a deteriorating economic situation, the Spaniards do not engage in the development of new businesses. 100 Spanish entrepreneurs surveyed said the same thing – they blamed the government for the current situation, because not only does it not care about them, it also makes them feel like outcasts. Still, the Spanish government has already taken measures and is preparing an action plan similar to the U.S. JOBS Act to increase the number of new businesses in the country.

The differences between countries demonstrate how important it is to understand that the government of the country has to take care of tax, financial and other assistance in order for a competitive mindset to begin to flourish. Startups will not be born in a country if it does not pay sufficient attention to involving and supporting an educational system that produces engineers, mathematicians and IT professionals.

The individual focus of each EU member state on startups allows one to see and understand how much creative inspiration a country has, or whether conditions are favourable for implementing it. It is possible to distinguish between countries that are developing potential from those that have universities, research institutes and absorb EU funds, but basically rotate within the same economic potential which was created in the past and is more or less related to the development of intellectual potential (for example, newly found oil deposits).

Baltic countries

The Baltic countries have two leaders: Finland and Estonia. Once having been one of the top mobile phone manufacturers, being Nokia is no longer pleasing for the Finns. They find it strange that the once famous company, Rovio, developer of the Angry Birds game, has released it for other phones first. Therefore, a Slush conference is organized in Finland every year as compensation to help startups gain momentum. Its initiator is Rovio's marketing director, Peter Vesterbacka.

At the last Slush conference, Jyrki Katainen, the Finnish Prime Minister said: Many people say that the downfall of Nokia was the best thing that could happen to our country, because it will allow us to come up with new ways and means to ensure well-being, and it will be a basis to thrive on.” Some people even say that the current downfall of Nokia is the best thing that has happened to this country because it's challenged us to come up with new ways to create a foundation for our welfare. Katainen also vowed that the Finnish government would do everything to help startups, starting with tax cuts for business angels and venture capital funds, to capital allocation for technology centres.

Estonia boasts that it is the country with the highest number of startups in the world per capita. Everyone has heard of Skype, but here are some the country’s latest startup gems: TransferWise has attracted 6 million U.S. dollars in investment, and Fits.me, 7.6 million U.S. dollars. A total of 28.6 million U.S. dollars in venture capital was invested in Estonia last year.

Other Baltic countries are not doing so well. Lithuania can only boast of a few success stories: GetJar and Pixelmator. Latvia has its Latvian Mark Zuckerberg, Lauris Liberts, managing the Draugiem Group – the only social network in Europe that has withstood Facebook.

In assessing the current situation in the Baltic countries, it should be noted that Lithuania, Latvia and Estonia in particular, are quite successfully moving along the path in their promotion of startups and thereby enhancing their growth potential. Investors should take note of this, because if more startups grow within the next year, long-term positive developments will open up before our eyes that will have a significant impact on investment return.

Consider whether what U.S. President Obama is doing is a proper example that could be applied to other countries. Maybe the U.S. economy is not like the Greek economy only because it has chosen the path of developing startups. Are the countries that you want to invest in doing the same thing?

Article excerpt:

A study made in 2013 funded by the Kauffman Foundation reveals that from new jobs created every year, as many as 70 percent are created by companies that have been operating for less than a year. The Forrester Research study suggests that as many as 78 percent of small companies and startups believe that they will expand over the next two years, and as much as 39 percent of them hope to double the number of employees.

The winner of the year: Chinese Renminbi

"It's all for money and goods, this fighting and quarrelling" (Pieter Bruegel the Elder, 1570)

The Third Plenum of the 18th Central Committee announced a comprehensive programme of reforms that will support China’s ambitions to develop into a global superpower by the end of the decade. China is envisioned to become more market-oriented, competitive, liberal, transparent and investor-friendly. In other worlds, China will continue to go along the path of Westernization, which, symbolically, has started precisely 35 years ago during The Third Plenum of the 11th Central Committee Congress led by a legendary reform leader Deng Xiaoping. The strategy proved to be highly successful: in 1978 China’s economy was more than ten times smaller than that of the USA and produced only 2% of global economic output, whereas in 2018 China is forecasted to surpass America to become the largest economic power generating 18% of the world’s economic output. These impressive achievements more than anything else motivate Chinese political elite to keep the Western direction.

And yet the fact that China becomes like the West, by no means suggest that China likes the West. China is becoming similar to its Western counterparts in virtually every dimension except one – political system. In spite of economic liberalization, People’s Republic of China was, is and will continue to be ruled by the Communist Party. Hence, political rivalry between the West and China ought to intensify in line with growing Chinese economic power. China’s plans to create an air defence identification zone around Japanese controlled Senkaku (Chinese: Diaoyu)islands were immediately followed bya “Cold War-like” rhetoric from Pentagon. The incident perfectly illustratesthe existing tensions between China and the West that at times reminds us of the Cold War antagonism: the difference is that this time it is China and not the Soviet Union that represents the East. However, this time the battlewill not be about who will get the larger number of nuclear warheads.To paraphrase the inscription of Pieter Bruegel the Elder “It's all for money and goods, this fighting and quarrelling”. China already flooded the world with “made in China” goods, but stable and freely convertible currency is a necessary prerequisite in order to successfully compete in global financial industry. China perfectly understands that and is ready to fire off a principal weapon: Chinese Renminbi, which is actually ready to compete with US dollar and euro, even though it will not be an easy task in the world controlled by the Western powers.

The West rules the rest

The year 1991 was the year of triumph and victory for the Western World. The Collapse of the Soviet Union ended the Cold War and greatly increased ideological and military dominance of the USA and its Western allies. Symbolically, the same year witnessed the collapse of Japanese real estate market that put anend to a post-war Japanese economic miracle. With Soviet Union and Japan defeated, the West set off to dominate the world. America de-facto became the world policeman, whereas united Germany became the economic powerhouse of newly created European Union (Maastricht treaty was signed in 1992). China was a no match for the West at that time: its economy was no larger than that of France, Italy or … the State of California.

The year 2001 marked two attempts to question global dominance of the West. The September 11 attacks challenged military and ideological supremacy of the West. Just a few months later, British economist Jim O'Neill coined an acronym “BRIC” (Brazil, Russia, India and China) – a group of emerging powers that supposedly were eager and ready to challenge Western economic dominance. And yet neither terrorists nor BRIC posed a real threat to the Western World. The War on Terror gave a nice “excuse” for the USA to carry on its world police duties. Economically BRIC countries, although making a good progress, were no match for the West as well. The GDP of all BRIC states combined were still significantly lower than that of the USA or European Union alone. China was still seen as a place to produce cheap “made in China” goods whereas Russia continued to lose its influence in Eastern Europe to rapidly expanding European Union and NATO.

In fact, the largest threat to the West was the West itself. Excessive confidence and optimism led to excessive borrowing, which eventually led to global financial and economic crisis in 2008. The situation looked increasingly serious and reminiscent of the Great Depression. When credit boom suddenly went to bust, many countries were forced to impose strict fiscal discipline, while consumers massively cutback their spending fearing that the worst it still to come. With domestic consumption trapped into the vicious credit cycle everyone gave high hopes on exports to drive their economies out of the recession. The temptation to start “Beggar Thy Neighbour” type of competitive currency devaluation policies was extremely high as were the stakes. But there were precisely these “strategies” used by many countries that delayed economic recovery after the Great Depression and resulted in multiple armed conflicts in late 30’s. The world seems to have learned this lesson: the Currency War did not happen this time and precisely this no-happening allowed international trade and global economy to recover.

Currency War that did not happen

English proverb says: “A friend in need is a friend indeed”. And the best friend of the Western world during the economic crisis was China. Not only China did not embark into the Trade Wars with the USA or the European Union, but it also did not succumb to the temptation to devalue its currency in times of economic distress. China is occasionally being accused by the USA of implementing competitive devaluation practices that allegedly give Chinese producers an unfair competitive advantage over the American producers. But in fact it is not so much about China as about the USA itself.

To begin with, China’s current account surplus was a mere 1.3% in 2001, but as the USA started implementing ultra-loose monetary policy things started to change dramatically. Too cheap and too easy credit transformed Americans into the real “homo-consumericus” – to paraphrase Rene Descartes, the motto of American consumers became “consumo ergo sum” (“I consume, therefore I am”). Cheap and abundant “made in China” goods, German cars, Taiwanese computers, Saudi Arabian oil and American dream houses – all those purchases made USA current account deficit to widen from 3.7% in 2001 to 5.7% in 2006. China benefited a lot from this consumption frenzy in the USA. In just 6 years, Chinese current account surplus increased almost tenfold reaching an impressive 10% of GDP in 2007. But China was not alone. For example, Germany has increased its current account surplus from 0% in 2001 to 7.5% in 2007. So did Saudi Arabia, Sweden, Israel, Malaysia, Japan and other export-oriented countries that managed to avoid USA-like consumption boom (Spain, Greece and the Baltics were among those that did not). Hence, blaming China for growing global trade imbalances during the pre-crisis period wouldn’t be objective. Especially keeping in mind the fact that China removed the peg in mid-2005 and allowed the Renminbi to gradually strengthen against the US dollar from mid-2005 until mid-2008.

But even more important is that China decided not to weaken Renminbi during the global economic crisis in 2008 and instead allowed it to strengthen in line with the US dollar (which was strengthening vis-à-vis other currencies due to its status of save haven currency). This action had a profound effect on increasing attractiveness of Chinese Renminbi. First, doing this China made a clear signal that it will not start currency wars with its trading partners. Hence, China proved that it can be a reliable and trustworthy trading partner for the West. Secondly, China effectively transformed Renminbi into a safe haven currency i.e. anchor of stability that is sought after by international investors in times of economic crisis. By choosing not to devaluate its currency and re-pegging it to the US dollarinstead, China in fact sent a signal for international investors that Renminbi is at least as strong as the US dollar in times of turbulence. Thirdly, China’s action illustrated growing divergence between China and the rest of BRIC countries. Since the onset of the crisis the currencies of Brazil, Russia and India significantly weakened against the US dollar. Brazilian Real and Russian Rouble were particularly hard hit and lost close to 60% of its pre-crisis value while Indian Rupee depreciated by 30%. Chinese Yuan, on the contrary, gained in value until mid-2008 and then remain fixed vis-a-vis US dollar until mid-2010.

Renminbi: at least as strong as the US dollar

In fact, global economic crisis in 2008 wasn’t the first time Chinese Renminbi proved itself as an anchor of stability. During the 1997 Asian financial crash most South-East Asian countries devaluated their currencies, but Chinese Renminbi on the contrary - appreciated. This helped other Asian countries to regain their international competitiveness at the expense of China. For example, current account balance of Thailand, Malaysia, Philippines, South Korea and Indonesia turned from negative one in 1997 to positive one in 1998 and the years to follow. On the contrary, China’s trade deficit with ASEAN countries turned negative in 1998, while the total current account surplus gradually declined from 3.9% in 1997 to 1.9% in 1999 and further on to 1.3% in 2001. Were China to follow the example of other countries and devaluate Renminbi, recovery in South East Asia would have been undermined. But China decided not to devalue and instead even allowed Renminbi to strengthen symbolically. Hence, the first test was passed in 1998, the second one – in 2008, and the third, decisive one, in 2013.

In May 2013 FED announced that the era of economic stimulus (money printing) is going to an end. Warren Buffet once rightly remarked that “you never know who's swimming naked until the tide goes out” – and with FED’s announcement the tide of easy money expectations suddenly all but vanished. As a result of that,currencies of all the BRIC countries weakened against the dollar except one: Chinese Renminbi. In just four months Indian Rupee, Brazilian Real and Russian Rouble depreciated by 22%, 19% and 7%, whereas Chinese Renminbi on the contrary – appreciated by 1%. It shows that Renminbi is building up credibility as safe and stable currency that tends not to lose value in times of economic turbulence – property so needed and sought after by international investors. Hence, contrary to other currencies of BRIC countries, Chinese Renminbi fulfils the necessary condition to become one of the global reserve currencies. China’s case becomes even stronger keeping in mind the fact that Japan – its long-standing rival in Asia – is implementing Abenomics economic policy as a consequence of which Japanese Yen depreciated significantly… It’s now Japan and not China who would rightly deserve accusations of encouraging global currency war. Especially given that current account surplus in China dropped to 2.2% of GDP in 2013 and is expected to narrow further to a mere 1% in 2015.

Making Renminbi global

An yet, keeping stable exchange rateis definitely a necessary, but by no means a sufficient condition to become global reserve currency. It is financial liberalization that is needed. The ruling Chinese Communist Party was unwilling to liberalize financial markets fearing that foreign capital inflows and cheap capital could destabilize domestic economy. However, The Third Plenum of the 18th Central Committee seems to be a game-changer. Measures have been announced that in less than a decade could potentially make Chinese Renminbi among the top three global reserve currencies. There are two ways in which China will liberalize and globalize Renminbi: gradual widening of trading bandaround the official fixing rate determined by the People's Bank of China and experiment with Shanghai (andpossibly Guangdong) free trade zones.

First way: Gradual widening of trading band

Prior to mid-2005 Renminbi was fixed to US dollar with occasional devaluations to retain international competitiveness of Chinese manufacturing production and keep trade balance in surplus. For example, China’s trade balance moved into negative territory in 1993 and was immediately followed by Renminbi devaluation the year after. However, devaluation of Renminbi in 1994 proved to be the last one, since improving productivity and rising export volumes helped China to keep international trade surplus. Hence, the Renminbi remained fixed to the US dollar until mid-2005 when significant trade surpluses started to accumulate threatening the stability of the global trade. As a result, China decided to unpeg Renminbi from the US dollar and introduced a managed float regime. Specifically, Renminbi was allowed to fluctuate +-0.3% around the official fixing rate determined by the People's Bank of China. The band was widened to +-0.5% in 2007, +-1.0% in 2012 and is expected to be widened further on to +- 1.5% in the beginning of 2014.It is important to mention that between mid-2008 and mid-2010 Renminbi was temporarily re-pegged to the US dollar, but this event did not change the general tendency for Renminbi to gradually increase its exchange rate flexibility and eventually transform Renminbi from fixed to floating currency – an essential feature aiming to become global reserve currency.So far, the experiment goes smoothly: Renminbi gradually but surely appreciates against US dollar approaching 6 Renminbi per US dollar mark (the rate was 8.27 when the peg was abandoned in mid-2005).

However, more freedom for currency necessitates more freedom for financial market as a whole. First, capital controls should be gradually lifted. For example, China imposes limits on the amount of foreign currency an individual can take in a given year. Existing regulation is that each individual is not allowed to take more than 50000 US dollars per year. However, these regulations become superficial given that many people find ways to bypass the law. In addition, the recent upsurge of the usage of virtual global currencies, such as Bitcoin, could make these restrictions even harder to enforce. Another issue is interest rate liberalization. Under existing regulation, commercial banks’ deposit rates cannot exceed the benchmark deposit rate set by the People's Bank of China by more than 10%. For example, one year benchmark deposit rate currently stands at 3%, hence, Chinese savers can receive for their one-year deposits no more than 3.3%. China also used to impose similar limits on lending rates, but those restrictions were removed in July 2013. And yet, it will be a real challenge for China to eradicate deposit rate control, since it would seriously hurt banks’ profitability and may potentially destabilize Chinese financial system, which is dominated by state-owned banking groups. Hence, this road to Renminbi globalization will be gradual and potentially with some set-backs if experiments do not bring desired results.

Second way: Shanghai free trade zone

At the same time China is moving in other direction in trying to make Renminbi more freely convertible and used by international community. On September 2013, China opened up the Shanghai free trade zone with no restrictions on capital movement and interest rates. The experiment is expected to last three years and if it proves to be successful thecapital and other controls will be gradually lifted in other provinces and later on – on a national scale. In fact, Shanghai is already not alone as Guangdong free trade zone is expected to be opened in early 2014. If those experiments succeed, China expects to liberalize Renminbi by the end of 2015. Hence, as soon as in 2016 a powerful rival will come to global stage with an aim to challenge US dollar and euro and together Western absolute dominance in the world of money.

The battle for money: ChinAmEurica

The Cold War between the West and the Soviet Union left the world littered with dangerous nuclear warheads. On the contrary, Sino-American rivalry will leave it covered with “made in China” goods, US dollars and Chinese Renminbi. It’s because China and America are like newlyweds firmly tied into the marriage of convenience. China is the biggest creditor of the USA, whereas the USA is by far the biggest export partner of China. This simply means that America without China would experience severe financial crisis, whereas China without America would delve into deep economic crisis. However, as Benjamin Franklin once put it “Where there's marriage without love, there will be love without marriage”. Love, after all, is not war and this is very good news for the global economy. To paraphrase anti-war slogan of the Cold War period, the Sino-American rivalry will “make money, not war”. Europe and the rest of the world can greatly benefit from this battle; hence, contrary to the situation during the Cold War, countries should strive to get into the front line of this battle.

The battle for money between China and the West will make both parties more prosperous. On one hand, China’s rivalry won’t allow the West to become overly complacent and relaxed. Rivalry is a necessary condition for capitalism to flourish – and China is the perhaps the best country to take over the role of a key competitor. On the other hand, increasing pressure from the West will prompt China to speed up reforms and challenge the West in the world of money and finance. China clearly understands that and seems to be ready to globalise Renminbi as soon as in 2016.

Finally, China, together with the USA and European Union, is supposed to become one of the three global powers, responsible for safeguarding stability and prosperity of the global economy. And yet, the fight for ChinAmEurica as a new world order for decades is not going to be easy for anyone.

Lithuanian investment in Belarus: success and failure

Sowing Success

1. Vakaru medienos grupe & SBA

On 28 February 2011, UAB Vakaru medienos grupe (VMG) and the Republic of Belarus signed an investment agreement on the implementation of the investment project “Establishment of a vertically integrated wood processing complex in Mogilev region in the territory of Mogilev Free Economic Zone”. The foreign limited liability company VMG Industry, founded and registered as a resident of the Mogilev Free Economic Zone in June 2009, was selected for implementing the investment project. The investment project involved investments in fixed assets totalling EUR 58.264 million, and attracted EUR 64.3 million worth of Lithuanian investments to Belarus and resulted in the creation of at least 870 new jobs. The investment project was financed by the European Bank for Reconstruction and Development and a few German banks.

Also on 28 February 2011, the foreign limited liability company Mebelain (an SBA group company) and the Republic of Belarus entered into an agreement on implementing the investment project “Construction of a furniture manufacturing facility in Mogilev Free Economic Zone”. Mebelain was registered as a Mogilev FEZ resident back in April 2010. The business plan of Mebelain’s investment project provided for investments in the amount of EUR 15 million (including EUR 8.2 million investments in fixed assets), setting up to 270 new jobs and the export of 100% of the goods it produced.

At the beginning of July 2013, Vakaru Medienos Grupe and SBA successfully opened an industrial complex worth more than LTL 325 million in the Mogilev FEZ. The joint project is going to be one of the largest foreign direct investments in Belarus by Lithuanian investors.

VMG Industry representatives emphasize that the easy access to raw materials (timber) and their good relationship with the local authorities of Mogilev were important factors that determined their investment decision. Initially there was great uncertainty as to whether Belarus would let a furniture manufacturer in the country, however, the plans for exporting considerably facilitated the negotiation process. A joint venture of furniture manufacturers enables efficient communication with suppliers and reduces logistics costs. According to the representatives of SBA group, the purpose of the factory in Belarus is to consolidate SBA’s position in Eastern markets, where they see a strong potential for development and growth in consumer purchasing power. At the same time, as a part of the Customs Union, Belarus provides better opportunities for Mebelain to sell its products in CIS countries with its considerable resources of raw materials and an old furniture manufacturing tradition.

2. Arvi group

Arvi group has two investment projects in the Lida District in the Grodno region of Belarus worth EUR 27 million in total.

The first project, valued at about EUR 20 million, envisages the building of a turkey meat production facility. The company plans to produce up to 5,000 tonnes of finished products per year. This will be a vertically integrated facility engaged in turkey breeding (about 420,000 turkeys per year), production of combined fodder (about 40,000 tonnes), slaughterhouse activities (6,000 tonnes of live weight turkeys), and production of finished and semi-finished turkey products. The project is going to be localized in Belarus and will create 210 new jobs.

The second investment project involves the technical upgrade, renovation and capacity build-up of the Lida Veterinary Disposal Plant (with the project worth around EUR 7 million). An animal waste disposal facility will be built in the proximity of the Lida Veterinary Disposal Plant. It will boast top-notch equipment and technologies which will provide capability of producing up to 5,700 tonnes of tankage and up to 2,800 tonnes of inedible fat per year to meet domestic demand.

Both projects are financed by BPS-Sberbank and are anticipated to be implemented by 2017. The first output is expected to be produced in 2015.

Arvi’s top management believe that unexploited potential on the Belarusian market is vast due to very low levels of turkey consumption. Per capita annual consumption of turkey products in Belarus is less than 100 g, compared with nearly 3 kg in Lithuania. The investor believes that even reaching production volume of 1 kg per capita, meaning at least 10,000 tonnes per year, would be a great success.

3. Viciunai group

The Lithuanian surimi producer Viciunai group has invested in the construction of a seafood processing plant and logistic hub in Belarus. More specifically, two companies, Viciunai Bel and Viciunai Logistic, were registered in Belarus. EcoFort Company, one of Viciunai group companies, supplies and distributes frozen and chilled products under the Vici label on the local market and is a partner of the project. Initially, the capital to be invested was estimated at USD 5 million, while USD 3 million was planned to be invested during the first stage of the project of the logistic centre. The project of construction of the plant in Belarus was being developed for several years.

EcoFort sells Viciunai Group manufactured products in Minsk, Gomel, Mogilev, Brest, Vitebsk, Pollock, and Grodno as well as in other locations. The company represents Viciunai group trademarks VICI, ESVA, and Columbus. The company also represents international trademarks Dujardin (frozen vegetables) and Lutosa (frozen fries). The lion’s share of its sales in Belarus, serving 800 shopping outlets, comes from the sale of surimi products, breaded fish products and frozen pizzas (the market leader in pizza sales). Since 2006 crab sticks VICI have been annually winning the nomination “Choice of the Year”, while VICI pizzas were nominated for “Choice of the Year” in 2009.

Now Viciunai Group intends to move some of its manufacturing operations from Kaliningrad region, the Russian Federation, to Belarus. To that end, Viciunai Group has taken out a lease of land plots in the free economic zone in Belarus for the purposes of constructing a plant. Viciunai Group believes that its goods will reach customers in Russia’s major cities and in Kazakhstan one and a half days faster than from Kaliningrad region, because manufacturing in Belarus means fewer border crossing points that its goods have to pass through.

The Sting of Failure

1. Vladimir Romanov’s group in Belarus

In the mid-2000s the founder of Ūkio bankas, Vladimir Romanov, started doing business in Belarus. Sponsoring the MTZ-Ripo football club was one of the conditions for his investment project that he planned in Minsk. In 2005, Belarusian President Alexander Lukashenko approved Mr. Romanov’s investment project. Apart from building apartment houses in residential areas on the outskirts of Minsk, Romanov’s company ŪBIG planned to reconstruct Traktor Stadium, the second largest football arena in Minsk. The development plan included the construction of a shopping mall, a business centre, an indoor sports arena, a hotel, and a parking lot next to the stadium.

In 2007, an investment agreement was signed between ŪBIG and the Minsk City Council. Based on the agreement, the joint stock company (JSC) Stadium, an SPV, was established in order to implement the project. The SPV had to implement the development plan. The investment was valued at EUR 250 million.

The project was intended to be implemented until 2010, however, the construction of the complex was not even started. At the beginning of 2010, Minsk City Council terminated the investment agreement with Mr. Romanov. ŪBIG has been accusing Belarusian authorities of unreasonable delay of the project. According to public sources of information, it is most likely that the main reason for the conflict was the fact that instead of reconstruction of Tractor Stadium, JSC Stadium started to build residential houses in Minsk’s suburbs. When Belarusian authorities stopped supporting Romanov’s business, he announced his withdrawal from sponsoring FC MTZ-Ripo. The investment dispute will be heard before the International Court of Arbitration in Stockholm.

2. The Case of Vingės terminalas and Alvora in Belarus

In April 2013, the Belarusian company Belintertrans and UAB Vingės terminalas agreed on the commencement of the construction of a transport and logistics centre in the Volozhin Region, Minsk Oblast with the plans to spend an estimated USD 25 million. UAB Alvora, a major Lithuanian construction company with extensive experience of building logistics terminals, was to build the facility. The future transport and logistics centre was intended to service commodity traffic from CIS countries and Europe and to have offices, modern terminals for storage and customs clearance of cargoes. UAB Vingės terminalas announced that it was going to invest LTL 62 million in the logistics centre together with partners. The terminal would become one of the ten largest logistics facilities in Belarus and at the beginning of its operations was described as a model project of foreign investors.

The first construction stage was finished, however the second one was not even started, because a disagreement between the partners resulted in a big investment dispute heard before the Supreme Commercial Court of Belarus. The shareholders of the logistics centre operator Belvingeslogistik – UAB Vingės terminalas, UAB Alvora and Belintertrans, were accusing the counterparties of an attempt to push the partners out of the joint venture and take over the management of the logistics centre.

The Supreme Commercial Court of Belarus called for an amicable settlement between the parties, and it was announced at the beginning of March 2013 that Vingės terminalas had reached a verbal agreement with Belintertrans. At the same time the CEO of Vingės Terminalas stated that they would refrain from commenting any details until there is a document setting out how the agreement will actually be implemented.

Foreign direct investment: http://www.theglobaleconomy.com/Belarus/indicator-BX.KLT.DINV.WD.GD.ZS/

http://belarusdigest.com/story/wh-invests-belarus-13783

David L. Goldwyn and Leigh E. Hendrix: talking about economy

David L. Goldwyn and Leigh E. Hendrix

For Baltic Economy Magazine

US production of natural gas and crude oil from shale formations is transforming energy markets and geopolitics. The dramatic rise in US natural gas production has led to a rapid and sustained decline of US domestic gas prices, a revival of US manufacturing, a global glut of displaced liquefied natural gas (LNG) and a subsequent erosion in the linkage between crude oil and natural gas prices in Europe. Global gas markets are becoming more competitive and Middle East dominance of oil markets is increasingly challenged by the US and Canada. Shale formations are ubiquitous, so technologies that can produce them economically can democratize access to energy. Countries historically dependent on a single supplier, or on imported gas or coal, can access indigenous supply if the right economic framework is in place. So far, only a few countries have created such frameworks.

The US Experience. Since 2008, when the production of shale gas first garnered widespread attention in the United States, the US has experienced positive benefits with regards to price, climate and industry growth. US shale gas production rose from 2.25 trillion cubic feet (Tcf) in 2008 to a projected 8.6 Tcf in 2013.[1] The US is poised to become a net exporter of natural gas by the end of this decade. Today, natural gas prices in Europe average more than twice the average US price, while Asian gas importers pay roughly three times as much for gas. The US Environmental Protection Agency announced in October 2013 that carbon dioxide emissions from power generation declined by ten percent between 2010 and 2012 largely as a result of natural gas replacing coal as the power generation fuel of choice.

Impact on Global Markets. European markets began to see price improvements in 2008, when the US began producing enough shale gas to lower its imports of LNG, freeing up those LNG cargoes to go elsewhere, including Europe. Gazprom was forced to decide between adapting to new market realities or cede some of its market share. In 2012, a number of gas companies in Western European renegotiated long-term gas contracts with Russia’s Gazprom, including Poland’s PGNiG, Italy’s Eni, and Germany’s E.ON; some renegotiations resulted in retroactive price reductions.

US LNG exports are likely to grow, albeit slowly. The US is poised to become a net exporter of natural gas by the end of this decade, with some analysts projecting LNG exports of as much as six to eight billion cubic feet per day (bcf/d) by the end of this decade. So far, one export project has received final export authorization from the US government for 2.2 bcf/d and is currently under construction, while four additional applications, totaling 4.57 bcf/d, have received export approval conditional upon technical and environmental approval. The US Department of energy expects to issue new conditional approvals every two months, but final approvals can come up to eight months after conditional approvals, and if these projects reach final investment decision (not a certainty), construction can also take 2-3 years. It is safe to say that there will be LNG exports from the US, but the volume will be determined by market prices and the pace of development of competing LNG projects elsewhere in the world. As additional supplies of natural gas become available, whether as a result of US LNG exports or production of shale gas in Europe, Europe’s negotiating power will continue to grow.

Growing US oil production from shale impacts global oil markets. US production has helped to replace supply lost from Libya, Iraq, Sudan and Nigeria. US oil supply growth has helped lower the cost of security cooperation on Iran to China, Japan and Korea. The potential impacts of shale oil and gas development are enormous, particularly if the phenomenon can go global.

Can the Shale Gale Go Global? In spite of the positive market impacts to date, the benefits of shale oil and gas continue – so far – to be limited primarily to the US. Shale formations are ubiquitous, with resources being identified in Europe, Asia, Africa and South America. While Russia, China, the US and Argentina are among the largest resource holders for both shale gas and shale oil, there are sizable gas resources in European countries including France, Poland, and Ukraine, as well as Romania, Bulgaria and Lithuania. [2]

The U.S success is the result of the right configuration of geology, economics, technology, industry experience and policy. In 2008, natural gas prices in the US were relatively high, the resource plays were known, and the technological advancements in horizontal drilling and hydraulic fracturing made development economic. The domestic oil and gas service industry was robust, technically capable, and reputable. The US had in place an investment framework that helped to assure companies that they would see a return on their investment. And last but not least, the policy framework in the US, which included a stable regulatory regime, and land/mineral ownership rights, helped companies take the risk of investing. The scale of success in the US was dependent on all of those factors, and that success will be difficult to replicate.

Public Confidence. While US production has not been without controversy, the existence of sound environmental laws on drilling safety, water usage and emissions allowed US production to rise rapidly. Even so, our states created new laws on fluid disclosure, community impacts, water recycling and well bore integrity to address public concern over the scale of development.[3] In Europe and Latin America, shale oil and gas can be developed safely and successfully, but governments have to create policy frameworks to ensure safety and protect investment. Rules need to be robust and include rigorous enforcement mechanisms to engender public confidence. Numerous reputable organizations, not least of which include the International Energy Agency and Resources for the Future, have done work to outline how shale oil and gas can be developed safely, and their reports can help to provide a blueprint for designing sufficient regulatory frameworks. While safety and environmental protection are often the primary focus of regulatory efforts with regards to oil and gas development, governments also need to consider the issue of local benefits, which can be addressed through policies like revenue sharing or severance taxes. Additionally, development can be harder when there are entrenched interests that support the status quo in the energy sector, whether that be with regards to the fuel mix or supply hegemony. Governments can combat those interests by promoting diversity of supply and fuel types.

Investment Frameworks. Economics matter. Decisions to invest are driven by risk and reward. The cost of developing shale formations varies greatly based on geology and the availability of infrastructure. Tax and regulatory costs must incentivize exploration in early stages, as the risk of failure can be high. Unfortunately, some of the initial enthusiasm for shale gas development in Lithuania and Poland has waned, largely because the resources are proving to be too small or too costly to develop at current natural gas prices. In Central and Eastern Europe, oil and gas development can be particularly costly because there is limited existing infrastructure both for drilling and for delivering gas to markets. Given the numerous opportunities for natural gas development globally (including, but not limited to, unconventional gas), governments will need to be competitive in order to attract investment.

The Outlook for Europe. Misinformation, domestic politics and the lack of private ownership have slowed the development of shales in Europe so far. Those countries most dependent on imported gas from Russia have been the most motivated, led by Poland and Ukraine. Romania and Bulgaria have important resources, but internal political rivalries and some external desire to preserve market share have temporarily complicated development. In Western Europe, the United Kingdom has made major strides towards allowing the development of its shale resources in a safe and sustainable manner, evaluating the risks, working with industry to consider safe operating requirements, and being pragmatic about the timeline for development. Germany, which currently has a de facto moratorium on fracking, a formal moratorium is expected to result from recent coalition-forming talks among the leading political parties. Similarly, France currently has a moratorium on the practice of hydraulic fracturing. Russia, on the other hand, already a major player in the oil and gas world has substantial reserves of shale oil, providing them with a potential win in oil even as shale gas development elsewhere in the world is forcing them to adapt. So far, Russia has proven to be better able to adapt than expected, negotiating on fiscal terms and attempting to become more competitive. This will serve to make the Russian economy more competitive and, in the long run, less dependent on natural resources.

At present, no single European country has taken a leadership role with regards to developing a strong regulatory framework for shale development, and the EU Commission is not in a place to do so with such fragmented views among member states, and given the intensely local nature of allocation of water resources, land access and drilling safety. The US has taken a leadership role in promoting the safe development of shale gas through initiatives like the Department of State’s Unconventional Gas Technical Engagement Program, but global leadership on shale will have to extend beyond the US. The shale revolution should not just be an American tale- it should be a global opportunity.

In the end, the shale revolution strengthens global energy security and lowers the cost of carbon reduction. New supplies of oil and gas, be they from shale or from ultra-deepwater reservoirs or the Arctic, represent a slow democratization of energy that provides new countries with the chance to generate economic growth, improve their carbon intensity, and reduce the power of hegemonic suppliers. Even as incremental energy demand shifts from West to East, the world is becoming less dependent on energy production centered in an elite few countries. US LNG exports, and perhaps new supply from Canada, Australia and East Africa, will give counties more choice. In an era where ‘energy security’ remains critical to national security in Europe and elsewhere, this is an important shift, and one to be encouraged. But it will take good leadership to get the mix right.

Bios:

David L. Goldwyn is the President of Goldwyn Global Strategies, LLC. He formerly served as the Special Envoy and Coordinator for International Energy Affairs at the U.S. State Department, and as Assistant Secretary of Energy for International Affairs. Mr. Goldwyn is the co-editor of Energy and Security: Strategies for a World in Transition (Johns Hopkins University Press, Wilson Center Press: 2013) & Energy and Security: Toward a New Foreign Policy Strategy (Johns Hopkins University Press, Wilson Center Press: 2005).

Leigh E. Hendrix is an associate at Goldwyn Global Strategies, LLC., where she provides analysis on energy markets, trends and policy. She previously worked for the Energy and National Security Program at the Center for Strategic and International Studies.

[1] Energy Information Administration, “Annual Energy Outlook 2013,” April 2013 http://www.eia.gov/forecasts/aeo/source_natural_gas_all.cfm#netexporter

[2] Energy Information Administration, “Technically Recoverable Shale oil and Shale Gas Resources: An Assessment of 137 Shale Formations in 41 Countries Outside the United States,” June 2013 http://www.eia.gov/analysis/studies/worldshalegas/pdf/fullreport.pdf

[3] Resources for the Future, “The State of State Shale Gas Regulation,” May 2013, http://www.rff.org/centers/energy_economics_and_policy/Pages/Shale_Maps.aspx

Estonia: small, open and on solid ground

The performance of the Estonian economy since 2008 has to be seen within the larger regional context. With all major lenders belonging to Scandinavian banking groups and Nordic markets accounting for more than third of total exports, Estonia has become an integral part of an economic area that stretches from the Norwegian fjords to the expanses of Karelia and from the North Cape to the estuaries of the Oder and Vistula.

The northern dimension was particularly relevant during the immediate aftermath of the crisis, when domestic fiscal contraction was opportunely countervailed by the loose monetary policy of the Swedish central bank. Having the advantage of a flexible exchange rate, Riksbank responded aggressively by cutting its policy rates and letting the krona depreciate. While the financial markets impact of this on Estonia was fairly limited, the second round effects were probably rather significant. A weaker currency helped Swedish exports to recover at a brisk pace and that in turn enabled Estonian subcontractors to resume their sales. The end-result was the export-led rebound of 2010.

As for the euro pre-accession budgetary efforts, their impact should not be overestimated. For one, as a result of the long-lasting fiscal expansion, there was a great deal of froth in the system. Hence, the government was able to consolidate public finances by eliminating the worst excesses of the preceding boom and relying on ad hoc, one-off measures. That said, public payrolls and services were indeed cut. There crucial thing, however, was that due to the coming euro accession, the fiscal retrenchment was seen from the outset as a project with a fixed time frame and clearly-defined goal. This was no doubt instrumental in generating political support for this admittedly painful exercise.

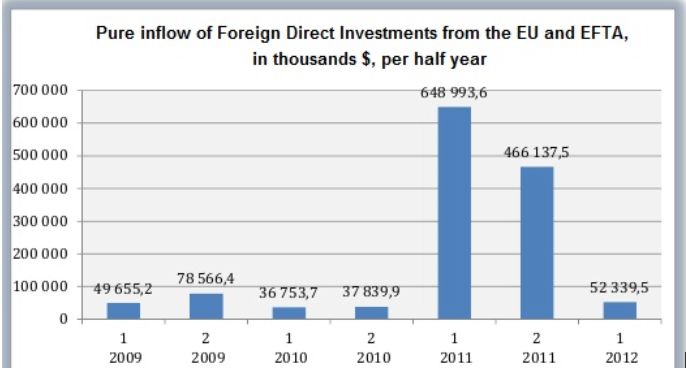

One of the main selling points of the common currency was its expected positive effect on foreign direct investment. After having turned negative in 2009 the net FDI flow did indeed recover strongly after that, and two years later the inflow was close to its all-time high. Since then, however, the interest of foreign investors in Estonian assets seems to have fallen once again, and in the last two years the inflows have fallen sharply. It is of course impossible to ascertain what role the euro has had in all this. On the whole, it seems reasonable to conclude that Estonia in the last years has been a beneficiary of the strong performance of the Swedish economy, which in turn is a satellites of the German economy – the unchallenged economic powerhouse of Europe.

Looking ahead there are perhaps two key issues to be aware of. First, there is a danger of getting caught up in the middle income trap. For the convergence process that had lifted Estonian GDP per capita from roughly one third of the EU average in 1995 to two thirds twenty years later, seems to have stalled. To the extent that there are plenty examples from around the world where countries get stuck at this level income, this scenario has to be taken seriously.

Secondly, the balance of payments data (see chart) reveal to what extent the recent recovery has been supported by the funds from Brussels. The cumulative outflow through financial account (decline in external liabilities) since the end of 2008 has amounted to 4 billion euros. Export boom notwithstanding, only a bit less than 1 billion euros have been earned back with foreign sales of goods and services. The rest of the 3 billion euro gap has been filled with capital account surpluses which capture mostly the inflows of European structural funds.

Hence, it is difficult to avoid the conclusion that the future of the Estonian economy depends to a large extent on the performance of the Northern European economies and on the continuation of the EU’s current budgetary policies. This is perhaps what being small and open ultimately means.

In the opinion of our editorial office, Hans H. Luik is a businessman that works in a particularly competitive and often problematic Baltic media market, which a host of famous media concerns have left, and has been able to not only survive, but be a leader. We chose him for an interview about economic trends and prospects on business expansion in the region because the media branches he leads demonstrate a rare high-level professionalism and objectivism.

The first thing that I would like to ask you would be your understanding of what happened in Latvia, Estonia and Lithuania after the crisis period. Could you say that these countries started to act differently and that the Baltic countries became a better place for doing business?